Base year recalculation methodologies for

structural changes

Appendix E to the GHG Protocol Corporate Accounting and

Reporting Standard

Revised Edition

Version January 2005

Introduction

Making meaningful comparisons of emissions data over time is

an integral part of any

corporate GHG report that aims to be credible, transparent and useful to

stakeholders.

A prerequisite for such meaningful comparisons is a consistent data set over time, or

in other words, comparisons of like with like over time

. In order for this condition to

be fulfilled, the inventory boundary must be held consistent between those data sets

that are used for a direct comparison over time.

A base year is a reference point in the past with which current emissions can be

compare

d. In order to maintain the consistency between data sets, base year

emissions need to be recalculated when structural changes occur in the company

that change the inventory boundary (such as acquisitions or divestments).

In practice this task is often m

ore complicated than it appears on the face of it. This

guidance document is an appendix to the

GHG Protocol Corporate Standard

Revised Edition

(March 2004)

, and clarifies some of the issues around base year

recalculations that often create confusion.

Firstly, this guidance document deals with GHG inventory recalculations under the

so

-called fixed base year approach, which is essentially a fixed historical reference

with which to compare current emissions (see chapter 5 of the revised

Corporate

Standa

rd

). Different options for making recalculations are presented, and it is argued

that under the fixed base year approach, the overall comparison over time is not

affected by the choice of option, while one option is more practicable than the other.

The s

econd part of this document describes the application of the different options

identified in the previous section under the so

-called rolling base year approach

(see step 4 of chapter 11 of the revised

Corporate Standard

( Setting GHG targets ).

It inves

tigates the implications of different methods and concludes that the choice of

method can have a bearing on which emission sources are included or excluded

from the overall emissions comparison over time.

Thus, it will be important to transparently docum

ent the choice of method when a

rolling base year is used, especially as this can be relevant for the compliance with a

corporate target.

Base year recalculation methodologies for structural changes

Please send yo

ur comments and questions to Simon Schmitz at

2

1 Base year recalculation methodologies for structural changes

using a fixed base year

Chapter 5 ( Tracking emissions over time ) of the revised

Corporate Standard

describes how to establish a fixed base year and recalculate the emissions from

that year in case of structural changes.

After recalculations under the fixed base year approach, emissions sources from an

acquired company are included both with their emissions in the base year (when the

acquiring company didn t control these sources yet) and in the current years.

Similarly, emission sources from divested facilities/companies are excluded both with

their emissions in the base year (when they were still controlled by the divesting

company) and the current years.

As recommended in chapter 5,

emissions should be

recalculat

ed for the entire year

( all-year option), rather than only for the remainder of the re

porting period after the

structural change occurred (the pro-rata option). The all-

year option avoids having

to

recalculate

base year emissions again in the succeeding year.

This can be described as the all-year option, since the inventory includes e

missions

from all facilities from January to December at all times.

In contrast, the pro-rata option operates on a step-

by

-

step basis. After making the

first recalculation, the inventory excludes a portion of the acquired or divested facility

in at lea

st the base and current year s inventories, until the full recalculation is made

in the following year.

To illustrate, Figure 1 describes example Z: the acquisition by a company A of a

company B in the middle of the year on 30 June. Example Z assumes tha

t emissions

from January to June are always the same as emissions from June to December.

Company A

with boundaries as before the acquisition

has emissions of 10 t CO2

from year 1 (the base year) through to year 4. The operations which were Company

B

in year 1 (but are acquired by A in the middle of year 2), have 1t of emissions in

year 1, 2t in year 2, and 3t in year 3 and 4.

Figure 1:

Example Z

(acquisition)

10

1 2 3 4

Year

Company A

Company B

Emissions

Company A

acquires

Company B

in June of

year 2

1

2

3

3

Base year recalculation methodologies for structural changes

Please send yo

ur comments and questions to Simon Schmitz at

3

Using this example, Figure 2 then compares the all

-

year option with the pro

-r

ata

option, when using a fixed base year. It illustrates that there have to be two

recalculations when using the pro

-

rata option, after which the resulting time series of

emissions and thus the comparison over time, is equivalent to the all year option,

wh

ich only requires one recalculation.

Figure 2: An acquisition (example Z) under different fixed base year options

Using the pro

-

rata option, illustrated on the left of Figure 2, company A would

when

first reporting its year 2 emissions, report 11t, including only the emissions of B from

June to December in year 2 (assumed to be 1t for simplicity). In order to compare like

with like, it recalculates its base year emissions to 10.5 t, including in its base year

emissions again

only B s emissions from June to December (in year 1).

When reporting on year 3, A would then include emissions from January to

December from B, and in order to keep comparing like with like, would have to make

a second recalculation to its base year emissions, to include B s emissions from

January to June in year 1. This results in exactly the same time series and

comparison over time (in the middle) as under the all-year option, which is illustrated

on the right (see also the shaded rows in table 1 to see that both approaches arrive

at the same result). The all-year option is thus clearly more practicable than the pro-

rata one.

Table 1: An acquisition (example Z) under different fixed base year options

Year 1

(Base year)

Year 2

Year 3

Year 4

Company

A s emissions

(boundaries as in year 1)

10

10

10

10

Company B s emissions

(boundaries as in year 1)

1 2 3 3

Pro

-

rata approach

Company A s year 2 report

10.5

11

Company A s year 3 report

11

12

13

All

-year approach

10

10

110

1 2

Year 2 Report

1

2

Year 2 Report

1

2 3

Year 3 Report

.

5

1

2

3

1

2

Under the fixed base year approach, the pro

-

rata and

all

-

year methods have the same result. The timing of

the recalculation also ultimately does not

matter.

a) Pro

-

rata

b

) All

-

year

Emissions

1

Base year recalculation methodologies for structural changes

Please send yo

ur comments and questions to Simon Schmitz at

4

Company A s y

ear 2 report

11

12

Company A s year 3 report

11

12

13

Further differentiating methods for recalculation is possible when taking into account

the timing of recalculation. It is possible to make the recalculation only in the report

for the year after the structural change, i.e., as if the structural change had occurred

at the end of the year (this could be termed the year-after option). The default

option (if sufficient data is available) would be to make the recalculation already in

the report for the year of the structural change, i.e. as if the structural change had

occurred at the beginning of the year ( same-year option). Switching between these

two options does not influence the ultimate comparison over time under the fixed

base year, just as wh

en comparing the pro

-

rata and the all

-

year options.

2 Target base year recalculation methodologies for structural

changes

using a rolling base year

As described in chapter 11 of the revised Corporate Standard, the rolling base year

approach requires mak

ing recalculations of base year emissions only for the previous

year, since the base year with which current emissions are compared on a like with

like basis is always the previous year. The rolling base year is another title for

establishing a new base ye

ar every year.

As mentioned above, after recalculations under the fixed base year approach,

emissions sources from an acquired company are included both with their emissions

in the base year (when the acquiring company didn t control these sources yet) a

nd

in the current years. Similarly, emission sources from divested facilities/companies

are excluded both with their emissions in the base year (when they were still

controlled by the divesting company) and the current years.

This makes for an important difference to the rolling base year, since the rolling base

year minimizes both the inclusion of emissions data from non-controlled sources

(e.g., before these sources were acquired) and the exclusion of data from controlled

sources (e.g., before these sources were divested). In this way, under the rolling

approach, any comparison over time is purely focussed on emissions that were

actually controlled or owned by the reporting company.

1

However, the extent to which this is achieved is not exactly the same for each of the

possible rolling base year recalculation methods.

The point of this section is firstly to describe the application of each of these possible

methods, and to show that each of them has slightly different implications for which

data is included or excluded. Thus, unlike under the fixed base year, it does make a

difference to emissions comparisons whether the pro-rata or all-year method is used.

In addition, the timing of recalculations (using the year-after vs. the same-

year

option) can als

o change emissions comparisons over time.

The combination of these different options results in four possible methods for rolling

base year recalculations. The next two sub-sections describe the application and

1

These and other differences are described in Figure 14 of the revised Corporate Standard

(p.81)

Base year recalculation methodologies for structural changes

Please send yo

ur comments and questions to Simon Schmitz at

5

implications of these four methods, for an acquisition and for a divestment

respectively.

2.1

Recalculating a rolling base year for acquisitions

Table 2 builds on example Z and illustrates the four different methods of how a rolling

base year is recalculated to account for an acquisition.

Table 2

: Methods for recalculating a rolling base year (acquisitions)

Pro

-

rata

All

-

year

Same-

year

The new reporting boundaries apply

from the year 2 report onwards, but

year 2 emissions (and the recalculated

emissions from the base year 1)

exclude Jan-June of B s emissions.

The full recalculation is made in the

year 3 report.

The new reporting boundaries

apply fully from the year 2 report

onwards, and year 2 emissions

(and the recalculated emissions

from the base year 1) include all of

B s emissions

Year

-

a

fter

The new reporting boundaries only

apply from the year 3 report onwards;

year 3 emissions (and the recalculated

emissions from the base year 2)

exclude Jan-June of B s emissions.

The full recalculation is made in the

year 4 report.

The new reporting boundaries only

apply fully from the year 3 report

onwards, and year 3 emissions

(and the emissions from the

recalculated base year 2) include

all of B s emissions

Figure 3 illustrates how each of the four recalculation methods outlined in Table 2

would

be applied to example Z. Figure 3 also shows that each of the methods has

different implications for the overall comparison of emissions over time (comparisons

from year to year is what the arrows are indicating).

Base year recalculation methodologies for structural changes

Please send yo

ur comments and questions to Simon Schmitz at

6

Figure 3: An acquisition (example Z) u

nder different rolling base year methods

Why do the differences between methods matter under the rolling base year

approach? An explanation is given in Table 3 below. It shows that each method has

different implications in terms of whether the company includes emissions from

sources that were not owned or controlled by it.

.5

d) All

-

year/ year after

adjustment

10

10

10

1

2

a) Pro

-

rata/ same year

adjustment

3

3

1

2

2

b) All

-

year/ same year

adjustment

10

1

1.5

3

3

2

3

c) Pro

-

rata/ year after

adjustment

1 2 2 3

1 2 2 3

Emissions

Emissions

1 2 2 3 3 4

1 2 2 3

Year 2

Year 3

Report

Report

Year 2 Year 3

Report

Report

Year 2 Year 3 Year 4

Report Report Report

Year 2 Year 3

Report Report

Emissions reported by Company A after the a

cquisition

Base year recalculation methodologies for structural changes

Please send yo

ur comments and questions to Simon Schmitz at

7

Table 3 illustrates these implications by comparing what is included in A s inventory

reports under each method and what was really owned or controlled by

A (see Figure

4 for emissions from sources that A did control in respective years in example Z).

As a basis for the comparison in table 3, figure 4 describes the emissions from

sources that A did control in respective years in example Z. The actual emiss

ions

from sources owned or controlled by A are 10 in year 1 before the acquisition and 11

in year 2: only half of company B s annual emissions were controlled by A since it

was acquired in June of year 2. From year 3 onwards, company A fully controlled its

own operations and those of company B.

Figure 4: Emissions from sources controlled by A in respective years in

example Z

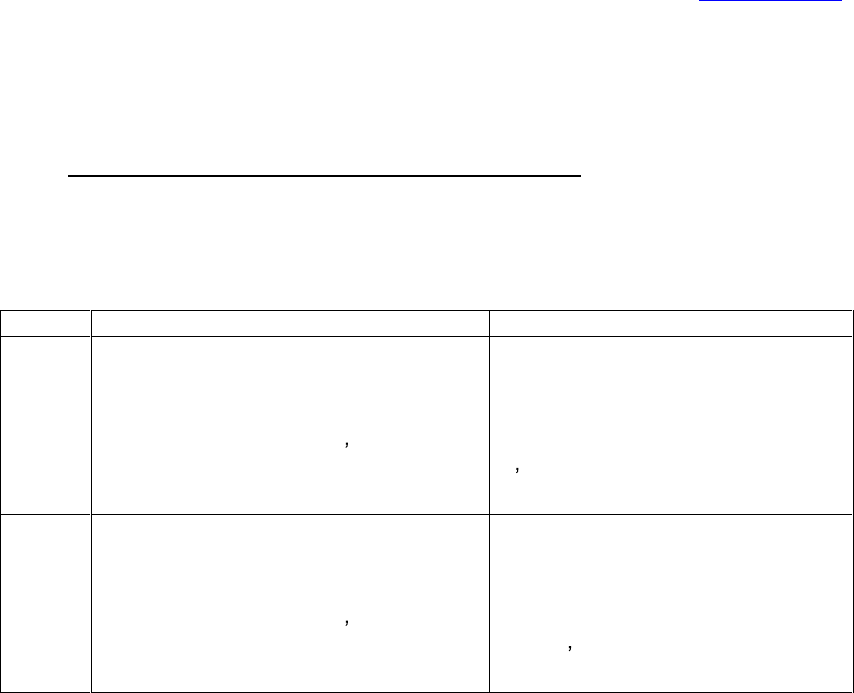

Table 3: Implications of different rolling base year recalculation methods for

acquisitions

Pro

-

rata

All

-

year

Same-

year

Half a year s data from B when not

controlled are included;

(No data from B when controlled

are excluded)

One and a half year s data from B

when not controlled is included;

(No data from B when controlled are

excluded)

Year

-

after

No data from B when not

controlled are included;

(No data from B when controlled

are excluded)

Half a year s data from B when not

controlled are included;

(No data from B when controlled are

excluded)

These differences in what is included or excluded can in turn result in different

comparisons over time under different methods. Thus, especially when setting and

reporting in relation to a GHG target using a rolling base year, it is important to be

transparent about which method is used, and to be consistent in the application of

that method.

In addition to making a difference to the overall comparison over time, the choice of

method also has implications for data requirements (the year-after methods usually

require data from the acquired company at a later stage than the same-year

methods).

1 2 3 4

Year

13

11

10

Base year recalculation methodologies for structural changes

Please send yo

ur comments and questions to Simon Schmitz at

8

2.2

Recalculating a rolling base year for divestments

The analysis of section 2.1 is repeated here for the case of divestments. Example Y

(Figure 5) is used in analogy to example Z: Company A divests a facility C

to

company B in the middle of year 2 on 30 June.

Figure 5: Example Y (divestment)

Table 4 builds on example Y and illustrates the four different methods of how a rolling

base year is recalculated to account for a divestmen

t.

Table 4: Methods for recalculating a rolling base year (divestments)

Pro

-

rata

All

-

year

Same-

year

The new reporting boundaries apply

from the year 2 report onwards, but

year 2 emissions (and the recalculated

emissions from the base year 1) still

include Jan-June of facility C s

emissions. The full recalculation is

made in the year 3 report

The new reporting boundaries

apply fully from the year 2 report

onwards, and year 2 emissions

(and the recalculated emissions

from the base year 1) exclude all

of C s emissions

Year

-

after

The new reporting boundaries only

apply from the year 3 report onwards;

and year 3 emissions (and the

recalculated emissions from the base

year 2) still include Jan-June of C s

emissions. The full recalculation is

made in the

year 4 report

The new reporting boundaries

apply fully only from the year 3

report onwards, but year 3

emissions (and the emissions from

the recalculated base year 2)

exclude all of C s emissions

Figure 6 shows how each of the recalculation methods wou

ld be applied in the case

of a divestment.

1 2 3 4

Year

Emissions

1

2

3

3

10

Company

A divests

Facility C

to

Company

B in June

of year 2

Emissions

from Facility

C

Emissions

from

Company A

ex

cluding

Facility C

Base year recalculation methodologies for structural changes

Please send yo

ur comments and questions to Simon Schmitz at

9

Figure 6: A divestment (example Y) under different rolling base year methods

Table 5 shows that each method has different implications in terms of whether the

company excludes emissions from sources that were actually owned or controlled by

it (and in fact in terms of whether the company includes emissions from sources that

were not actually owned or controlled by it any more).

Emissions

10

1 2 2 3

Emissions

10

1 2 2 3 3 4

c) Pro-

rata/ year after

adjustment

1

2

1

1.5

d) All year/ year

after adjustment

1

2

Year 2 Year 3 Year 4

Report Report Report

Year 2 Year 3

Report Report

Emissions reported by Company A after the divestment.

Each year is compared to the previous year s emissions.

Emissions

1 2 2

3

1 2 2 3

10

.5

a) Pro rata/ s

ame

year adjustment

1

b) All-

year / same

year adjustment

Emissions

10

Year 2 Year 3

Report

Report

Year 2 Year 3

Report Re

port

Base year recalculation methodologies for structural changes

Please send yo

ur comments and questions to Simon Schmitz at

10

It illustrates these implications by comparing what is included in A s inventory reports

under each method and what was really owned or controlled by A.

As a basis for the comparison in table 5, figure 7 describes the emissions from

sources that A did control in respective years in example Y. The actual emissions

from sources owned or controlled by A in example Y are 11 in year 1 before the

divestment and also 11 in year 2: half of facility C s emissions were controlled by A in

year 2 since the facility was divested in June of year 2. From year 3 onwards

company A only controlled its own operations without facility C.

Figure 7: Emissions from sources controlled in respective years by A in

example Y

Table 5: Implications of different rolling base year recalculation methods for

divestments

Pro

-

rata

All

-

year

Same-

year

No data from C when not controlled

are included;

Half a year s data from C when

controlled are excluded;

No data from C when not

controlled are included;

One and a half year s data from C

when controlled are excluded;

Year

-

after

One year s data (two halves) from C

when not controlled are included;

No data from C when controlled are

excluded

Half a year s data from C when

not controlled are included;

No data from C when contro

lled

are excluded;

These differences in what is excluded or included can in turn result in different

comparisons over time under different methods (as shown in Figure 5). Thus,

especially when setting and reporting in relation to a GHG target using a rolling base

year, it is important to be transparent about which method is used.

1 2 3 4

Year

11

10